It is worth mentioning that the overall bullishness of foundry has a lot to do with the rise of wafer ASP (average selling price). After all, in the market environment of lack of core, the price increase of foundry factory is quite common. Many enterprises have achieved substantial growth in performance under this wave tide

Semiconductor has a relatively long industrial chain, and the response of upstream to downstream will be relatively slow. As the upper reaches of the semiconductor industry, due to the previous large-scale lack of cores at the downstream application end, the overall trend of semiconductor manufacturing is still quite good even if some of the more downstream market demand is saturated.

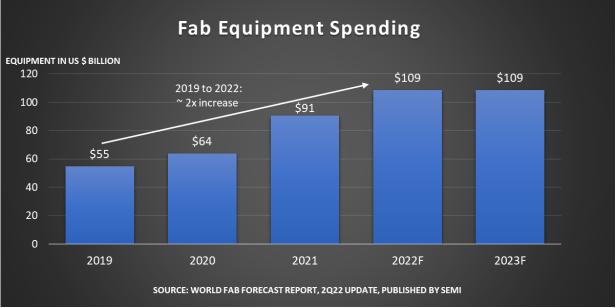

Further upstream, semi has given data in the latest world Fab forecast report. It is estimated that the investment in fab front-end manufacturing equipment and facilities in 2022 will reach $109billion, a new historical record and a breakthrough of $100billion for the first time. The year-on-year growth rate of 2022 has reached 20%. Although the year-on-year growth rate of 20% is slightly lower than that of 42% in 2021, if this forecast is correct, 2022 will become a sustained high-speed growth for three consecutive years.

Ajit manocha, President and CEO of semi, said: "this historical record has written an exclamation point for the current unprecedented sustained industry growth." It shows that the expected investment of 109billion yuan is still quite amazing. We will combine the data recently released by semi, Gartner and counterpoint research to see the current development of the semiconductor manufacturing (including its subsidiary foundry) market. This will help us understand the future trend of the whole industry.

Investment in manufacturing equipment is still rising, and Taiwan still ranks first

From the perspective of semiconductor manufacturing equipment, the semi report mentioned that this year, the global fab equipment expanded by 8% - compared with the growth rate of 7% last year. Semi believes that the growth of fab equipment market capacity will continue until 2023, and it is expected that the growth rate next year will be about 6%.

In history, the last year-on-year increase of 8% was in 2010, when the monthly production capacity of the wafer reached 16million (equivalent to 200mm wafer); It is estimated that this value will reach 29million tablets / month in 2023. In the semiconductor manufacturing equipment expenditure in 2022, 85% comes from the capacity growth of 158 Fab plants and production lines.

Geographically, Taiwan, China will still be the leader of Fab manufacturing equipment spending this year, and the investment in this area will reach US $34billion, a year-on-year increase of 52%; Followed by South Korea, an increase of 7%, with a specific value of US $25.5 billion; In the third place market in Chinese Mainland, according to semi, this year's investment in fab equipment will decline by 14% to US $17billion - which has a lot to do with the decline after last year's high growth.

At the same time, the investment in the European / Middle East market will reach a record US $9.3 billion, with a growth rate of 176%. In the Americas, the investment in fab equipment will increase by 13% and 19% year-on-year in 2022 and 2023 respectively, and will reach about US $9.3 billion in 2023. Semi believes that in 2023, Taiwan, China, South Korea and Southeast Asia will all have a relatively satisfactory rise in this regard.

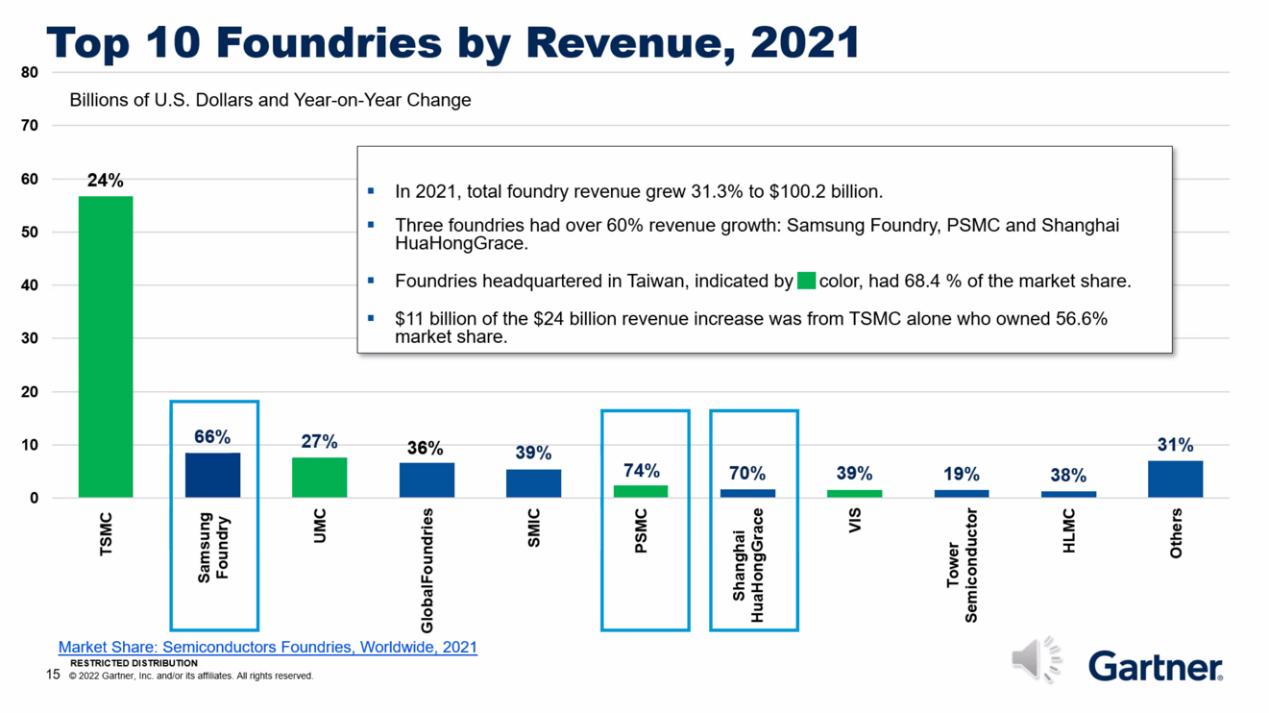

From the top 10 of foundry plant

In fact, the investment in manufacturing equipment in different regions is completely predictable. In the semiconductor industry report released by Gartner not long ago, it was given that the foundry plant ranked among the top 10 in terms of revenue in 2021 - although it is not the whole semiconductor manufacturing area, it can also reflect the current situation of the semiconductor manufacturing industry.

The top 10 foundries in terms of revenue include TSMC, Samsung, UMC, Globalfoundries, SMIC, PSMC, Shanghai Huahong Hongli, VIS, tower semiconductor and Shanghai hlmc. Taiwan, China, Chinese Mainland and South Korea are obviously the main forces.

The revenue of these foundry plants in 2021, even the tower semiconductor with the slowest growth rate, also increased by 19%; The revenue growth of market participants such as SMIC and Globalfoundries has even reached more than 35%; The three companies with the fastest growth in revenue are Samsung foundry, Li Jidian and Shanghai Huahong Hongli, with growth rates of 66%, 74% and 70% respectively.

Gartner mentioned that the main growth points of Samsung foundry came from the manufacturing of Qualcomm 5g chips, NVIDIA GPU and Google TPU, as well as the exaggerated demand for mining cards in the very hot mining machine market last year. The business growth of Li Jidian comes from DDI chips and some of its characteristic processes. The high-speed growth of Shanghai Huahong Hongli last year has a lot to do with the opening of Wuxi factory capacity and the substantial increase of overall capacity. Gartner also specifically mentioned that SMIC's 14nm process capacity has increased, which has become an important factor supporting revenue growth.

Of course, in terms of the absolute value of revenue, there is no foundry factory that can be compared with TSMC. The company's revenue last year exceeded $50billion, while none of the other nine top 10 companies exceeded $10billion. On the whole, the total revenue of foundry plant in 2021 will be USD 100.2 billion, with an average increase of 31.3%; TSMC contributed the most to the base.

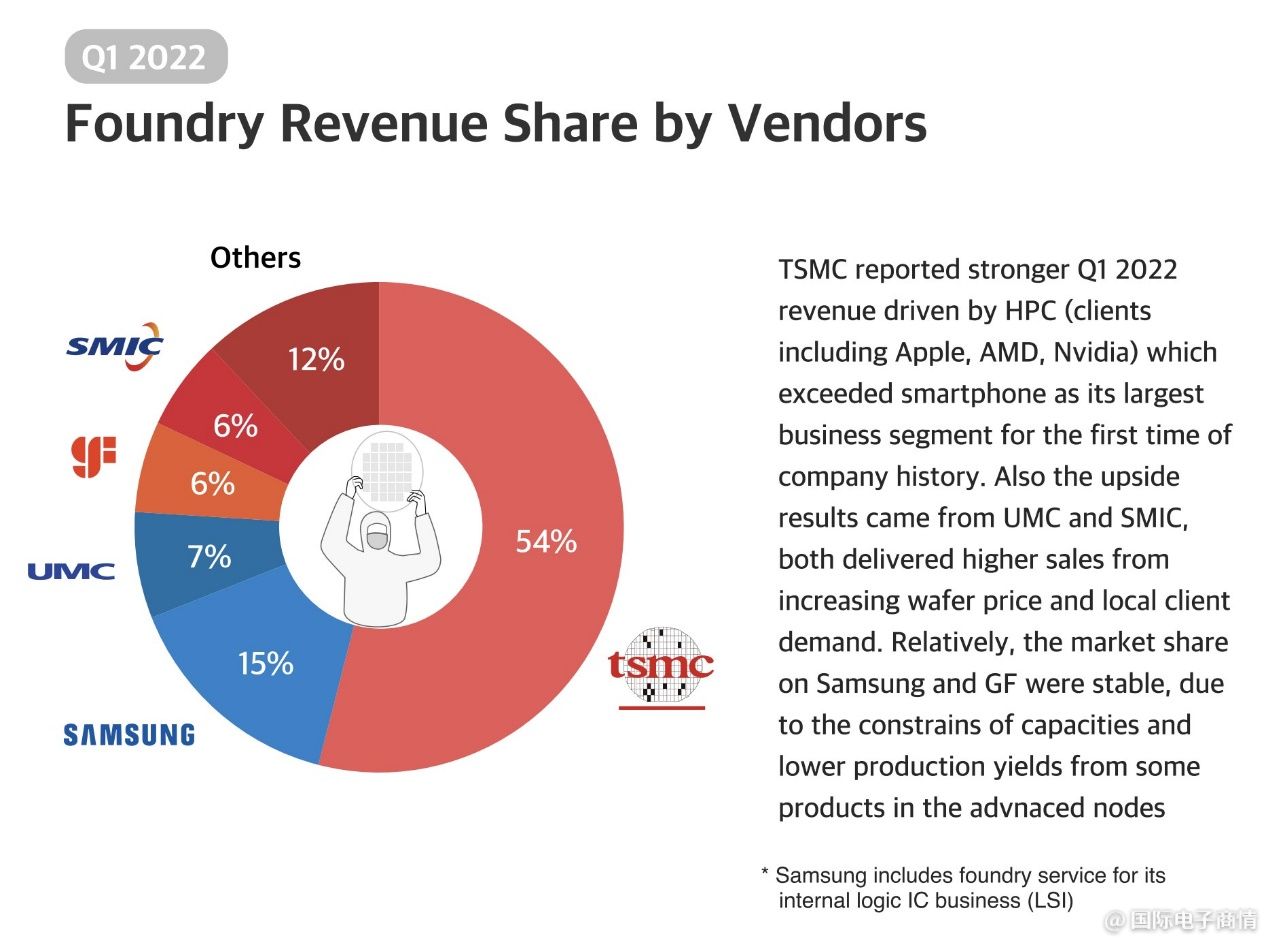

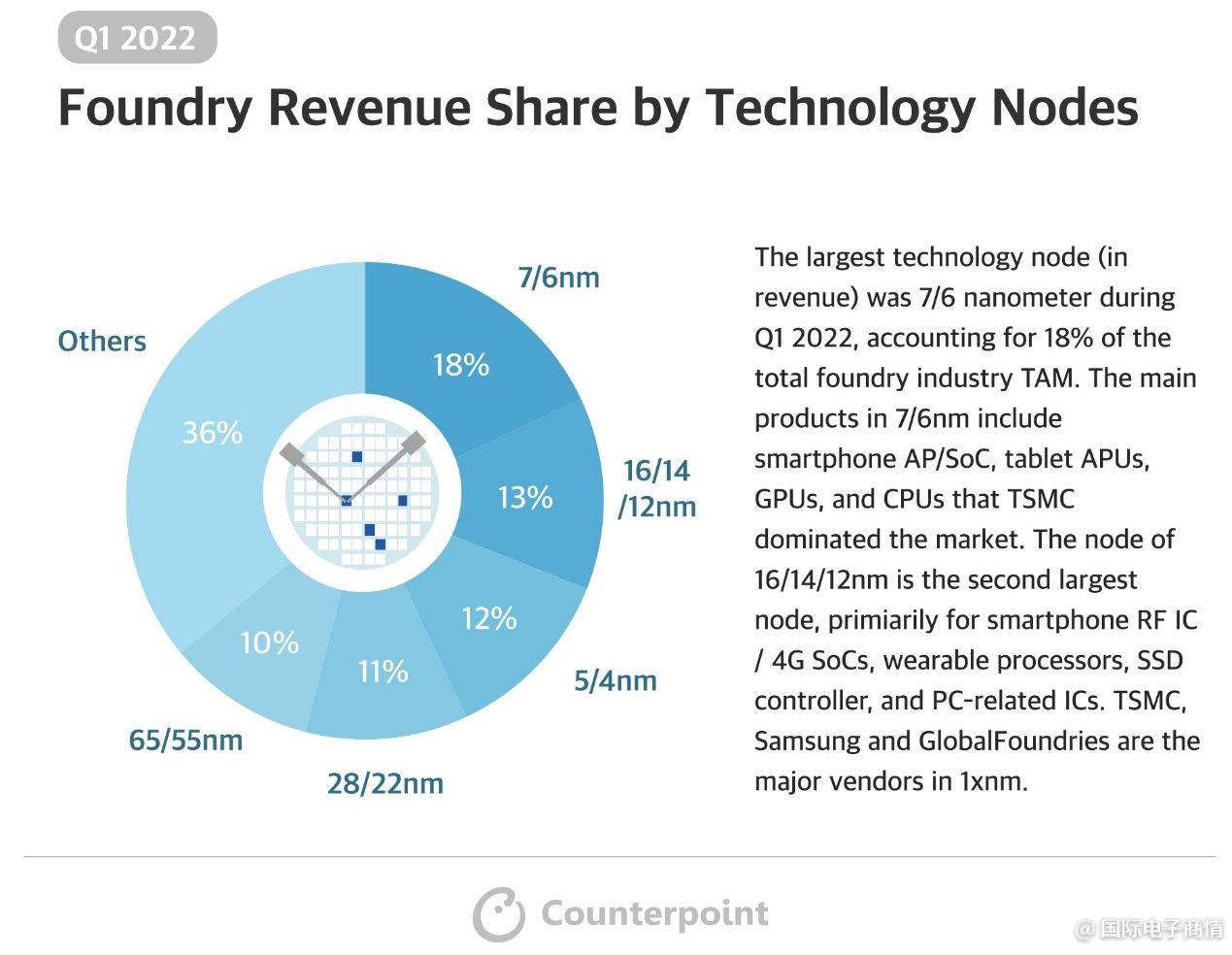

Recently, counterpoint research has just given the data of the proportion of the revenue of the foundation plant in 2022q1, as shown in the above figure. The overall situation is basically similar to that of last year. TSMC's Q1 financial report this year mentioned that its revenue was driven by HPC, including apple, AMD, NVIDIA and other customers; As we reported earlier, HPC has surpassed the smart phone business and become the most profitable application direction of TSMC.

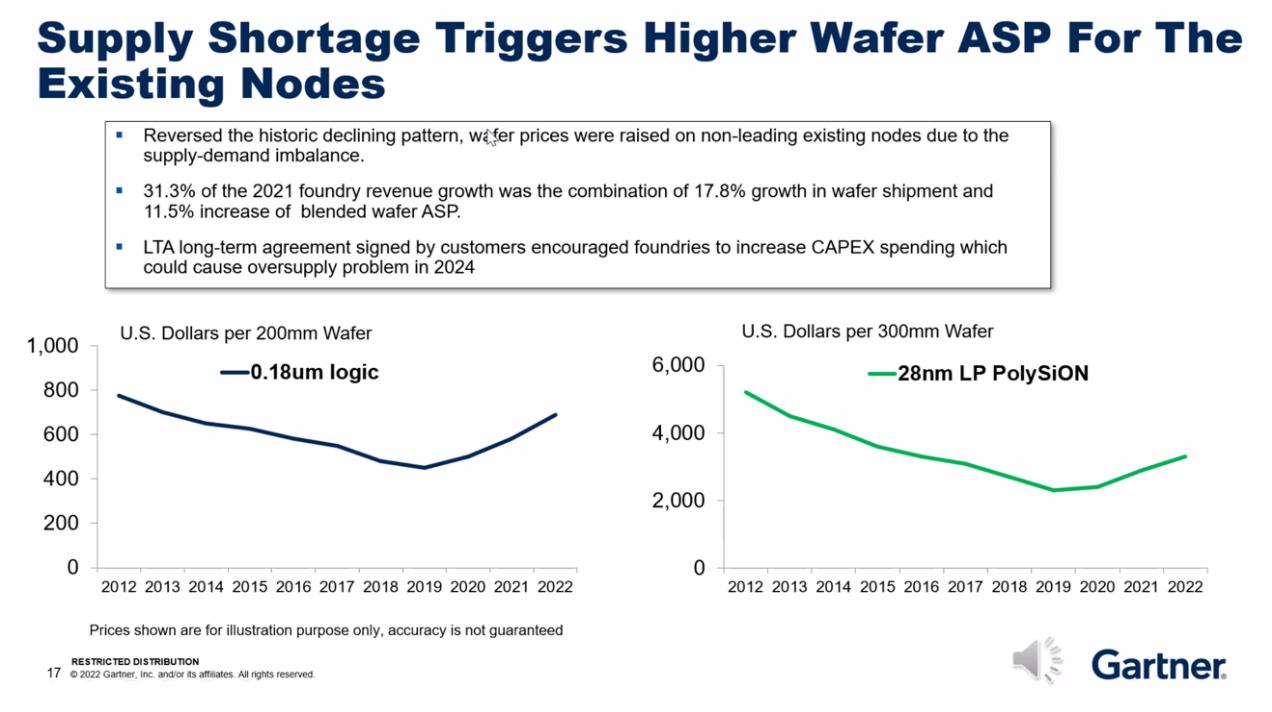

It is particularly worth mentioning that the overall bullishness of foundry plant is closely related to the rise of wafer ASP (average selling price). After all, in the market environment of lack of core, the price increase of foundry factory is quite common. Many enterprises have achieved substantial growth in performance under this wave tide, among which the more representative one, such as lijidian, still has a good grasp of the market.

The above figure shows the price trend of two different processes (and their corresponding 8-inch and 12 inch wafers) in the past 10 years. zero point one eight μ M and 28nm are also processes with large shipments. Such as 0.18 μ For 8-inch wafers of M process, the low price mainly occurred in 2019 - a year of overall decline in the semiconductor industry, and the wafer price fell below $500. Last year, its price has rebounded to close to or more than $800. The price trend of 28nm 12 inch wafer is also relatively similar, and the price of such mature process is also facing such an upward trend for a period of time.

The downstream customers of foundry, that is, chip design enterprises, have to accept the fact that the price of wafers rises during the core shortage tide - and because they are afraid that the price will continue to rise, they will sign some long-term agreements with foundry to ensure production capacity. As we reported earlier, the overall structural core shortage in the semiconductor industry is expected to end soon, although some areas will continue to lack cores; Due to the characteristics of the long industrial chain of semiconductors, the upstream foundry plants are still trying to seize the last opportunity of this wave of market.

Growth of different processes

According to the data released by counterpoint research, the process that 2022 Q1 accounts for the largest proportion of the revenue of foundry plant is 7nm/6nm, accounting for 18%. The main chip types under this process include smart phone ap/soc, tablet APU, GPU and CPU. 16/14/12nm has become the process with the second largest revenue (these processes are put together because they belong to the same process family). The main revenue sources are smart phone RF ic/4g SOC, wearable device processor, SSD controller and some PC related ICs.

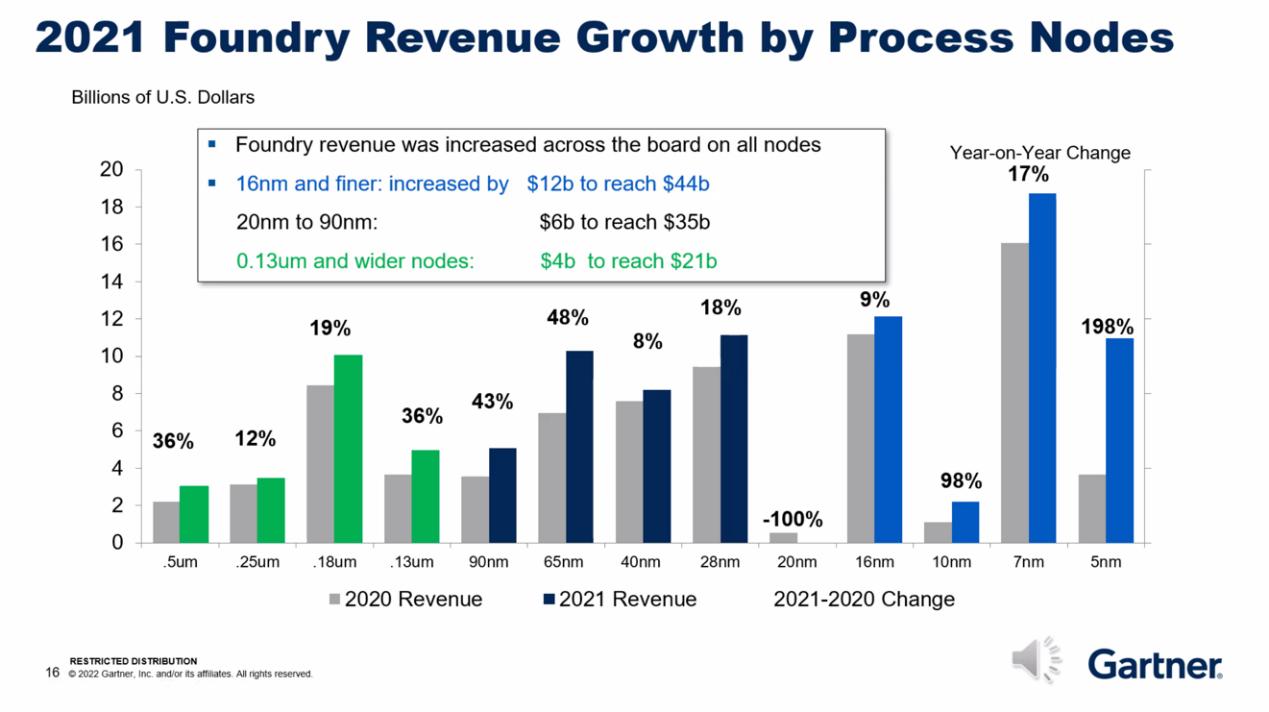

Gartner also recently provided the revenue growth of different processes in 2021. There is no doubt that the fastest growth in revenue is the 5nm process. The market value brought by the 5nm process in 2021 increased by 198% compared with that in 2020 - after all, it is the main force of the flagship mobile phone ap/soc chip, as well as applications such as Apple Mac chip. Gartner's data also shows that 7Nm currently accounts for the largest proportion of revenue among all processes - revenue growth has also reached 17% year-on-year since last year.

In 2021, the price increases rapidly, including many mature and traditional processes. For example, 28nm and 65nm. After all, MCU and other chips are in great demand. The revenue of 65nm process in 2021 increased by as much as 48% compared with that in 2020 - in fact, we can see the market demand.

The revenue of different processes depends on the investment of foundry. Gartner believes that the current investment scale of 28nm process is large, and the supply capacity of 28nm will increase significantly in the next few years. Among them, SMIC has plans to build 28nm factories in Beijing, Shanghai and Shenzhen. From the above figure, we can see the process investment bias of the current foundry plant, and understand the possible shortage or oversupply market trend. By the end of the year, we can see whether the supply of semiconductor products in different application markets tends to be saturated by looking at the revenue of different processes.

As a strong cyclical industry, the semiconductor industry has been inclined between different proportions of supply and demand. Unless the technological innovation ends, the rise and fall of the industry show cyclical changes repeatedly. The response of upstream semiconductor manufacturing to the market is relatively slower. At present, many chip categories are moving towards demand saturation. It should be different to observe the development of the semiconductor manufacturing market from 2023 to 2024.

Post time: Jul-12-2022